Industries: Banks, Fintechs

Authorized Push Payment (APP) fraud through social engineering isn’t a tech issue. It’s a human issue. Scammers trick users into sending money through pressure and artificial urgency. Enlace lets banks add smart friction at the right moment — stopping fraud without blocking real transactions.

To maximise fraud prevention, we need to break scams down step by step — from the fraudster’s perspective. Understanding their journey helps us place the right friction, in the right moment.

1. Stop targeting before it starts

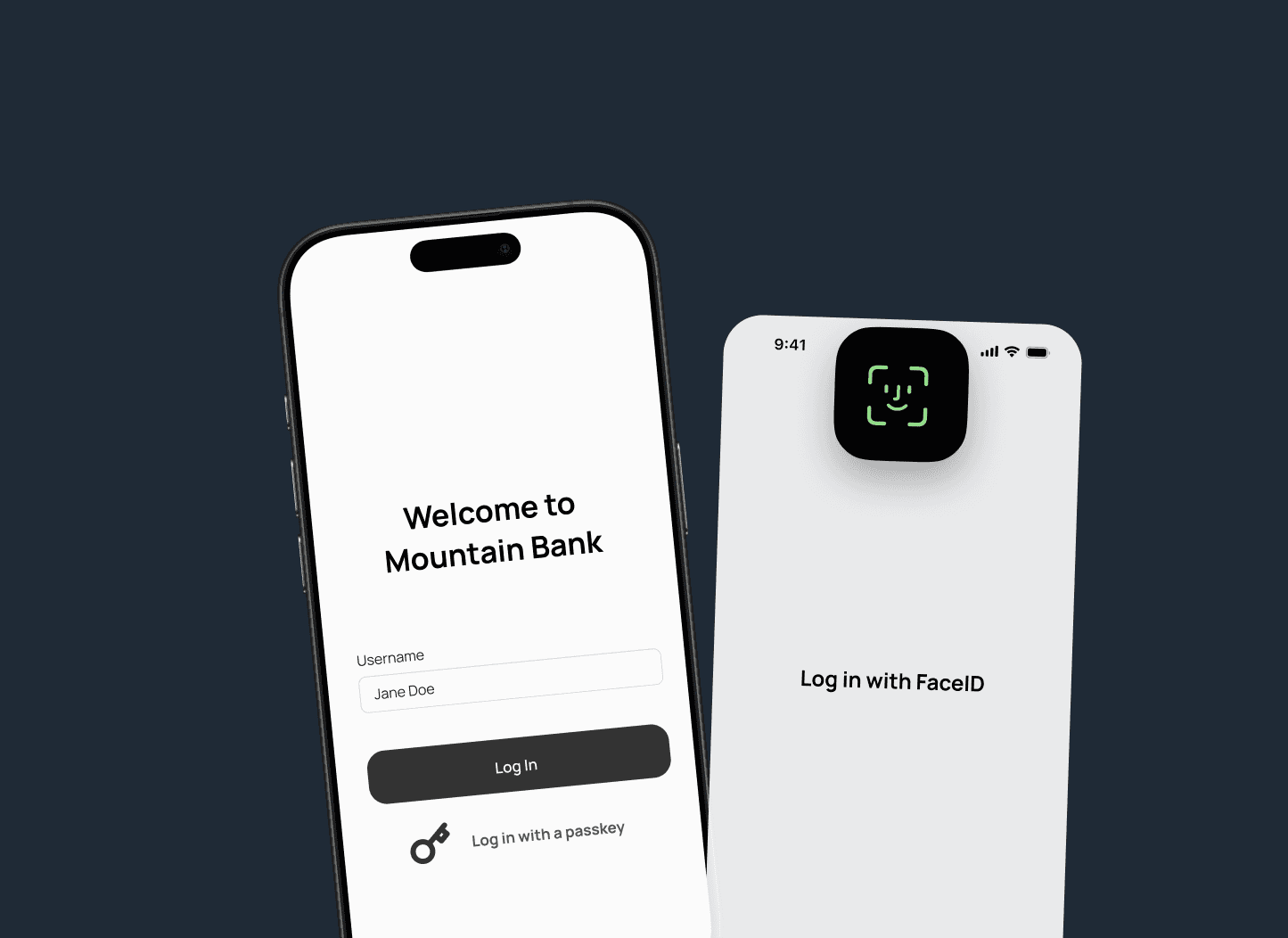

Fraudsters don’t start with the customer — they start with the bank. They scan for weak links like username-and-password logins and missing security layers.

Banks without strong protections become easy targets. And once the fraudsters are in, they know exactly how to exploit your users.

By adding friction where it matters — like risk-based step-ups and continuous checks — you make it harder for scams to take hold before they even begin.

2. Interrupt trust before it’s abused

Scammers sound like the bank. They spoof caller ID, reference real transactions, and guide users step by step — all to build trust fast.

Contextual in-app warnings help users spot something’s off. And with proactive education and outreach, banks can raise awareness before the scam even begins.

3. Disrupt artificial urgency with timely, targeted friction

Challenge

Fraudsters trick users into sending money by creating pressure and urgency. Traditional systems can’t detect these moments in real time.

Solution

With Enlace, banks can add smart friction right when it’s needed — helping users pause and think before they act, without disrupting genuine payments.

4. Cap payouts before the money moves

Once a payment’s approved, it moves fast — often through mules or overseas accounts. Recovery is rare.

Smart money-out limits cap high-risk transfers without blocking genuine ones.

Risk-based step-ups add an extra layer when something feels off. It’s a simple way to limit scams — and keep more money where it belongs.